Debt Counselling Fees - Debt counselling regulations 2019

One of the most frequently asked questions we get daily is what are the Debt Counselling Fees? South Africa dodged a recession in the second quarter with 3.1% growth. While we dodged a recession South Africans are adjusting to living in a country where unemployment and the cost of living are high. Research conducted by external companies shows that many South Africans are under pressure due to elevated debt rates. These consumers find themselves in this unfortunate situation and survive from payday to payday. According to another research found that financial stress causes mental and other health-related problems, therefore, consumers are turning to debt counselling to relieve the negative effects of being over-indebted leading to the most frequently asked question – what debt counselling fees are or what are the regulations governing debt review regarding fees.

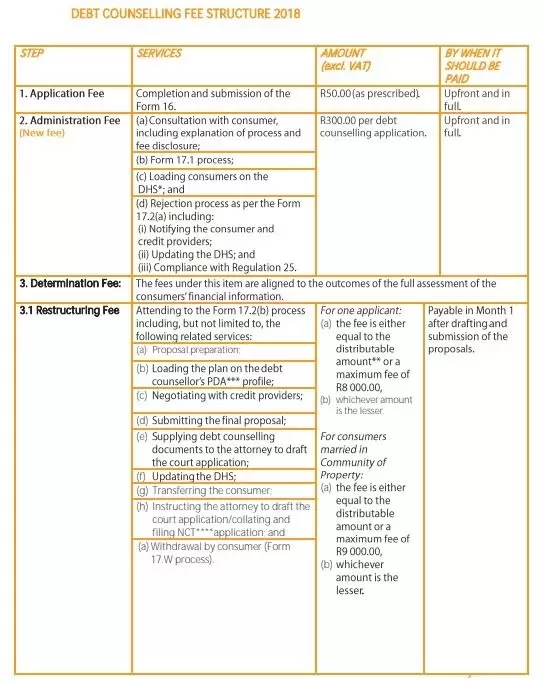

Debt counselling in South Africa is regulated by the National Credit Regulator and the National Credit Act. Debt Counselling is executed and performed by a debt counsellor who will negotiate with creditors on a consumer’s behalf. Debt Review aims to extend the duration of each credit agreement by reducing instalments and interest rates to assist debt-ridden consumers to pay off debt. Below are the standardized fees.

Step 1 - Regulations governing debt review - Application Fee

This is a flat fee to cover the costs of the debt counsellor to process the completed debt Review application.

Regulated Cost - R50

Payment Due Upfront and in full

Step 2 - Debt counselling fees - Administration

The second step in the debt review fee setup is the Administration Fee. The debt Review administration fee is a regulated once-off flat fee which gets charged by the debt counsellor. This fee is for administering the following processes:

- Consultation with the consumer. The consultation is the explanation of the Debt Review process and an explanation of the regulated fees.

- Notifications to credit providers advising them that the consumer has applied for debt review. Also, known as the Form 17.1 Process

- Capturing the consumers' details on the NCR Debt help system

- Attending any debt Review rejections (17.2 rejections) which will include

- Notifying the consumer and credit providers and the rejection

- Updating the NCR Debt help system

- Compliance with regulation twenty-five. Regulation twenty-five of the National Credit Act: If a debt counsellor finds that a consumer is not over-indebted and makes a finding in section 86(7)(a), the debt counsellor must provide the consumer with a letter of rejection

Regulated Cost – R300

Payment Due Upfront and in full

Step 3 – Debt Counselling Fees - Restructuring

The Fees under debt counselling are aligned to the outcomes of a full assessment of the consumers’ financial information and the following processes include:

- Proposal preparation for credit providers’ perusal

- Restructure the consumers' debt on the debt counsellors PDA profile

- Negotiations with creditor providers which include

- Negotiate reduced instalments

- Negotiate reduced interest rates

- Reduce or change insurances

- Submit final proposals to credit providers and the consumer

- Drafting, submitting, and supplying of debt counselling documents to attorneys to draft court applications.

- Updating the NCR Debt help system

- Attend to any transfer request from consumers

- Attorney instruction to draft court applications

- Filling of NCT applications in the cases of consent orders

- Attending withdrawal request from consumers (17.W process)

Costs – The restructuring fee is equal to the distributable amount of not more than R8000 for a single applicant and R9000 for consumers married in community of property

In other words, the first restructured instalment will get paid to the debt counsellor. The above limits apply

Example. Sally is in debt, and she earns R10 000pm after statutory deductions. She pays for rent, school fees, transport, and other expenses and for living expenses. In total Sally pays R4000 for all her debt.

Sally applied for debt review and her debt got restructured down to an amount of R2000. Sally is happy with this monthly amount as she can now afford to pay her living expenses and pay her debt. Sally made her first debt Review payment of R2000.

Payment Due: This first payment will get paid over to the debt counsellor for services rendered.

Step 4 – Reckless lending FEE

A debt counsellor will attend Reckless Lending Assessments and investigations and supply reckless lending documents to attorneys to draft affidavits on the assessment outcome

Cost: R1500.

Read More about reckless lending in our Reckless lending Blog Article and FAQ pages

Step 5 – After Care Fee

Debt counsellors will track your debt counselling progress and attend to the following while you are under debt review.

- Form 17.2

- Review of the consumers' financial situation

- Attend to any payment queries

- Attend the clearance process which includes securing paid up letters

- Attended the 17. W process. (Withdrawal from debt counselling by the consumer)

- Attending the update of the NCR debt help system

Costs: 5% of the distributable amount or an amount of not more than R450 per month.

When we go back to the Sally example: her new restructured amount to pay her debt is R2000. For the debt counsellor to track and attend to any queries Sally, the Aftercare fee will be 5% from R2000

= R100 aftercare fee.

Aftercare fees will never exceed R450. If the amount exceeds R450pm query the amount with the debt counsellor and the NCR.

Payment Due monthly will get deducted from the debt Review restructured amount.

Step 6 – NCT Submission Fee

A debt counsellor will submit your debt counselling application with the NCT to get a consent order.

Costs R500 once-off and this excluding the NCT filing fee. Currently, the NCT filling feeR200

Step 7 – Attorney Fees

The debt counsellor will appoint an attorney. We don’t make use of attorneys as we file with the NCT to save you costs. Should we need to approach the courts then this will be discussed up front and we will only proceed if you agree.

It is important to distinguish between debt review and administration. The above fees are for debt counselling and not for administration

Sources:

South African Government urges consumers to make use of debt review